A former partner at a16z issues a major technology report: How is AI devouring the world?

In his latest report, "AI Eats the World," renowned technology analyst and former partner at a16z, Benedict Evans, offers a judgment that is enough to shake up the entire tech world: generative artificial intelligence is triggering a massive platform migration in the tech industry every ten to fifteen years, and we still don't know where it will ultimately lead.

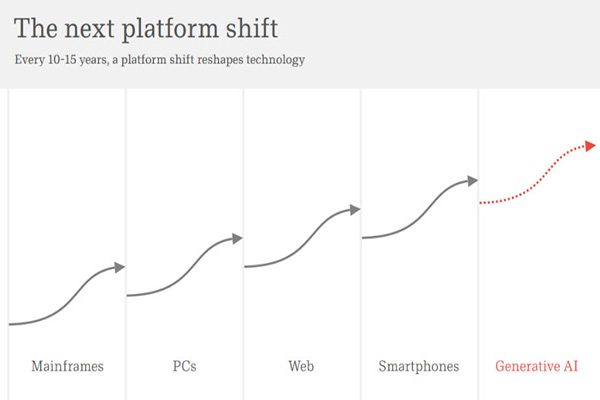

Evans points out that from mainframes to PCs, from the internet to smartphones, the fundamentals of the tech industry are completely rewritten every decade or so, and the emergence of ChatGPT in 2022 may well be the starting point of the next "fifteen-year shift."

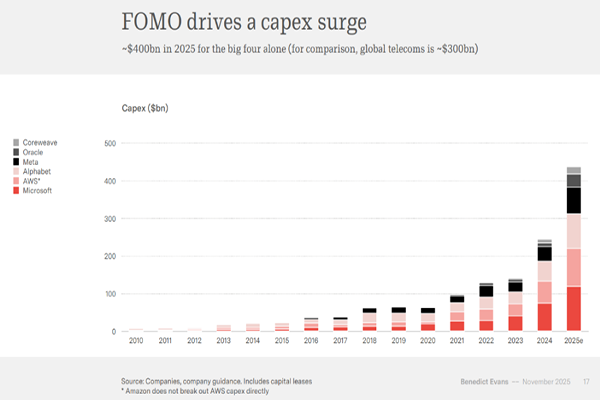

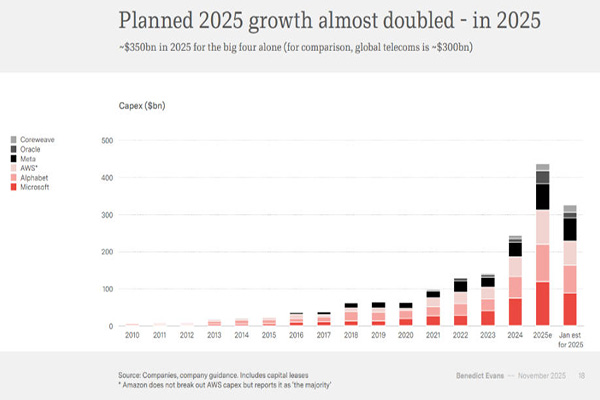

Global tech giants are embarking on an unprecedented investment race. The combined capital expenditures of Microsoft, Amazon AWS, Google, and Meta in 2025 are projected to reach $400 billion—a figure exceeding the approximately $300 billion invested annually by the global telecommunications industry.

"The risks of underestimating AI far outweigh the risks of overinvesting," a quote from Microsoft CEO Sundar Pichai cited in the report reveals the essence of the industry's anxiety.

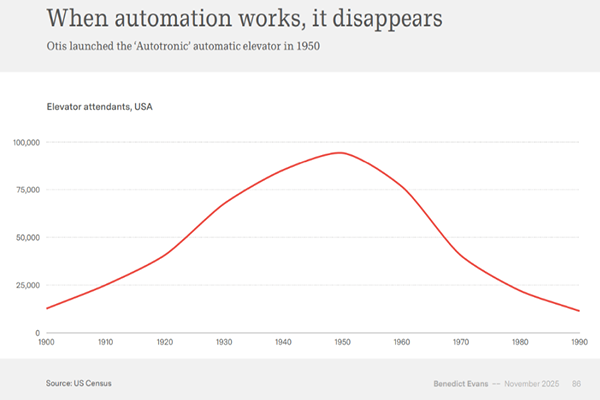

The report also cites the 1956 US Congressional Automation Report and the case of the disappearance of elevator operator jobs as reminders: when technology truly takes root, it quietly becomes infrastructure and is no longer called "AI."

Another Fifteen-Year Shift: The Historical Pattern of Platform Shifts

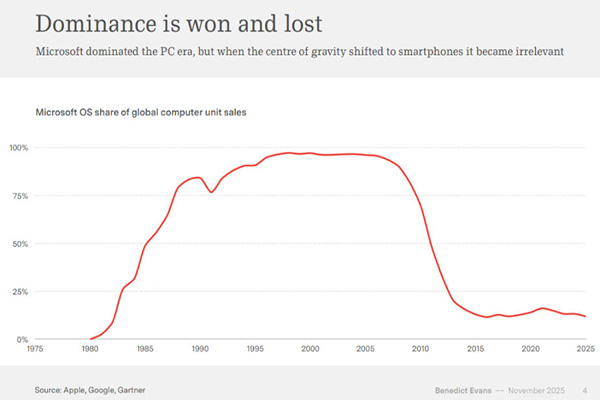

In his report, Evans points out that the technology industry experiences a platform shift roughly every ten to fifteen years, from mainframes to personal computers, from the World Wide Web to smartphones, each shift reshaping the entire industry landscape. Microsoft's case illustrates the harshness of this shift: the company once held nearly 100% market share in operating systems during the personal computer era, but became almost irrelevant when the focus shifted to smartphones.

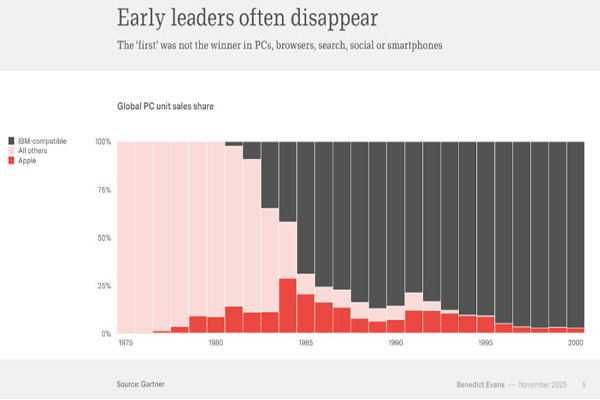

Data shows that Microsoft's operating system share in global computer sales has plummeted from its peak around 2010, and by 2025 it has fallen to less than 20%. Similarly, Apple, which dominated the early personal computer market, was marginalized by IBM-compatible machines. Evans emphasizes that early leaders often disappear; this seems to be an ironclad rule of platform shifts.

Three years later, however, little is known about the form this shift will take. Evans cited failed ideas from the early days of the internet and mobile internet, such as AOL, Yahoo! Portal, and Flash plugins. Now, with generative AI, the possibilities are equally dazzling: browser-like, agent-like, voice-interactive, or some entirely new user interface paradigm—no one truly knows the answer.

An Unprecedented Investment Frenzy: A $400 Billion Gamble

Tech giants are investing in AI infrastructure on an unprecedented scale. By 2025, the capital expenditures of Microsoft, AWS, Google, and Meta are projected to reach $400 billion, compared to approximately $300 billion annually in global telecommunications investment.

More notably, this growth plan for 2025 nearly doubled within the year.

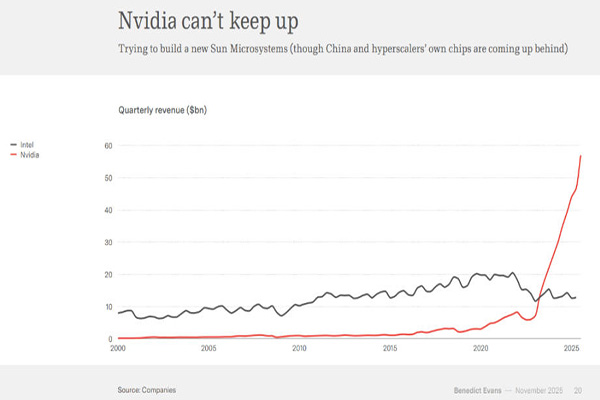

Data center construction in the US is surpassing office building construction in scale, becoming the new driver of an investment cycle. Nvidia faces supply bottlenecks due to its inability to keep up with demand, and its quarterly revenue has already exceeded Intel's accumulated revenue over many years. TSMC is also unable or unwilling to expand its capacity quickly enough to meet Nvidia's order demands.

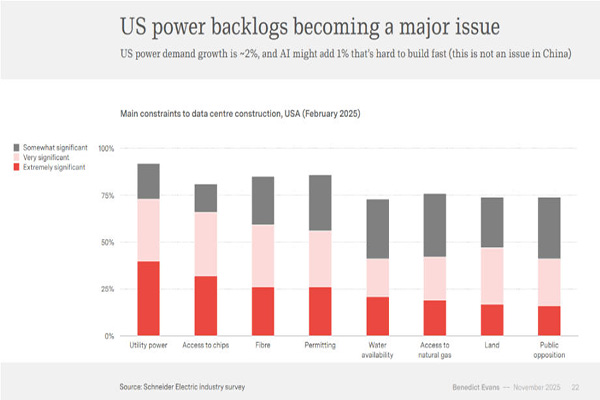

According to Schneider Electric's industry survey, the main limiting factor for data center construction in the United States is the public power supply, followed by chip supply and fiber optic access. U.S. electricity demand is growing by approximately 2%, while AI could add an additional 1% in demand. This wouldn't be a problem in China, but it's difficult to build rapidly in the U.S.

Model Convergence: Moats Disappear, AI May Be Becoming "Commoditized"

Despite massive investments, the gap between top large language models on benchmarks is narrowing to single-digit percentages. Evans warns:

If model performance becomes highly convergent, it means large models may be becoming "commodities," and value capture will be reshuffled.

In the most general-purpose benchmarks, the gap between leaders is already very close, with model leadership changing weekly. This suggests that models may be becoming commodities, especially for general use.

Evans points out that after three years of development, there has been significant progress in science and engineering, but a clear understanding of the market landscape remains lacking. While models continue to improve, with more models emerging, Chinese vendors participating, open-source projects appearing, and new technology acronyms appearing, moats are not yet clearly defined.

In his view, AI companies must rediscover their competitive advantages in areas such as computing power, vertical data, product experience, or distribution channels.

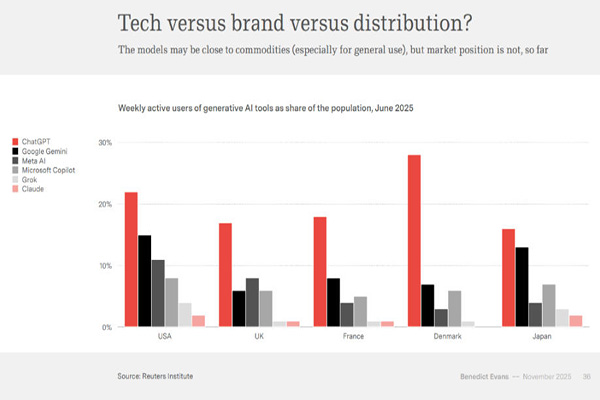

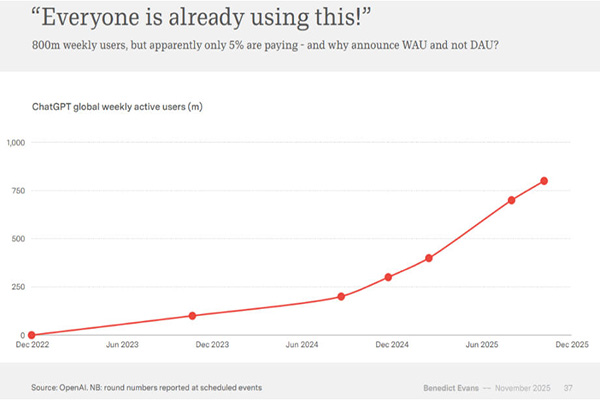

User Engagement Dilemma: ChatGPT's 800 Million Weekly Active Users Cannot Mask Insufficient True Stickiness

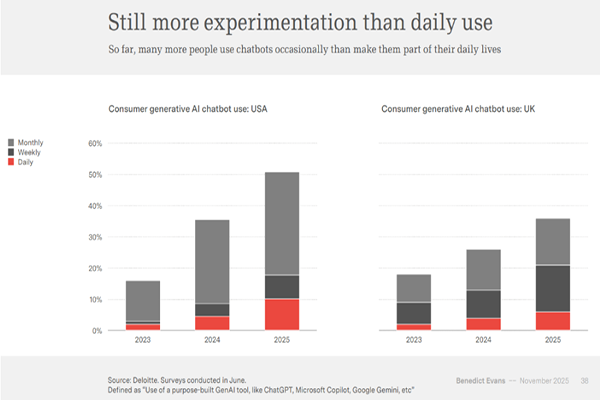

Although ChatGPT claims to have 800 million weekly active users, user engagement data paints a different picture. Multiple surveys show that only about 10% of US users use the AI chatbot daily, with most still only occasionally trying it out.

Deloitte's research data shows that the number of people who use AI chatbots on a daily basis is far greater than the number of people who use them only occasionally.

Evans calls this a classic "engagement illusion": AI is penetrating at an astonishing pace, yet it hasn't become a ubiquitous everyday tool.

He analyzes the reasons for this engagement dilemma: How many use cases are obviously easy to adapt? Who has a flexible work environment and is consciously seeking optimization methods? For others, is it necessary to package AI into tools and products? This reflects a significant gap between technical capabilities and practical application.

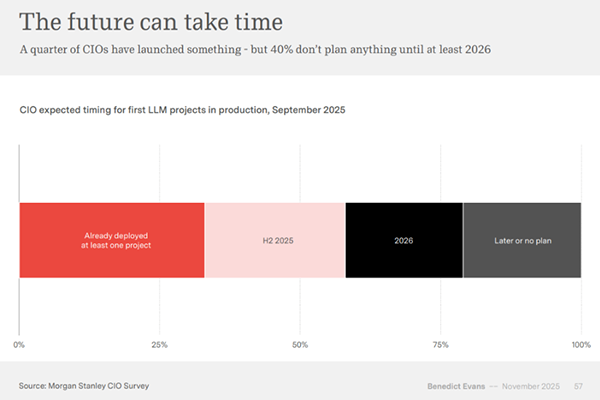

Enterprise deployment is equally slow. The report cites surveys from multiple consulting firms showing that despite high enthusiasm for AI among enterprises, few projects have actually entered production environments.

Deployed: 25%

Planned deployment in the second half of 2025: Approximately 30%

Deployment not until at least 2026: Approximately 40%

Current success stories are still concentrated in the "absorption stage," encompassing areas like programming assistance, marketing optimization, and automated customer support, and are far from true business restructuring.

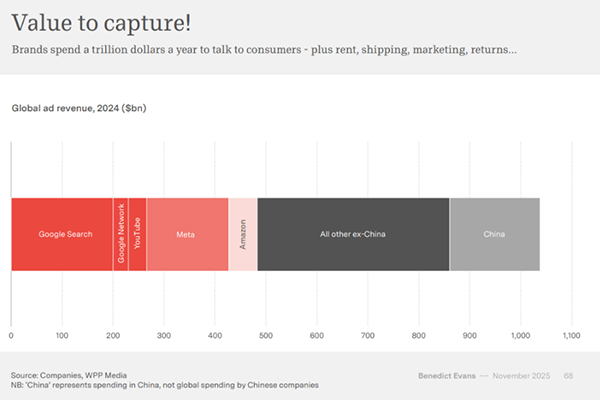

Advertising and Recommendation Systems Undergo Disruptive Rewriting

Evans believes that the area where AI will most rapidly and significantly change is advertising and recommendation systems.

Traditional recommendations rely on "relevance," while AI has the ability to understand "user intent" itself. This means:

The underlying mechanisms of the trillion-dollar advertising market may be rewritten.

Google and Meta have already disclosed early data showing that AI-driven ad delivery can lead to a 3%–14% increase in conversion rates. The cost of creating advertising creatives may also be further reshaped by automated generation technology, moving beyond the current $100 billion annual market.

Historical Lesson: When Automation Succeeds, It Is No Longer Called "AI"

Evans draws his attention back to the 1956 U.S. Congressional Automation Report, pointing out that each wave of automation sparked huge social debates, but ultimately quietly integrated into the infrastructure.

The disappearance of elevator operators, the inventory revolution brought about by barcodes, the transformation of the internet from a "new thing" into infrastructure… all prove that:

When technology truly takes root and benefits everyone, people will no longer call it "AI."

Evans emphasizes that the future of AI is both clear and ambiguous: We know it will reshape industries, but we don't know the final product form; we know it will be ubiquitous in enterprises, but we don't know who will dominate the value chain; we know it requires massive computing power, but we don't know where growth will stop.

In other words, AI is becoming the protagonist of a new fifteen-year cycle, but the entire drama is still unwritten.

We may be standing on the fault line of the next technological earthquake.

The Future of Value Capture: From Network Effects to Capital Competition

For research-intensive and capital-intensive commoditized products, value capture becomes a key issue. If models become commodities and lack network effects, how will model labs compete?

Evans proposes three possible paths: expanding downstream to win through scale, expanding upstream to win through network effects and products, or finding new dimensions of competition.

Microsoft's case illustrates a shift from competition based on network effects to competition based on capital acquisition capabilities. The company's capital expenditure as a percentage of sales revenue has risen sharply from historical lows, reflecting a fundamental change in the competitive landscape.

OpenAI has adopted a "say it or not" strategy, encompassing infrastructure deals with Oracle, Nvidia, Intel, Broadcom, and AMD; e-commerce integration; advertising; vertical datasets; and a diversified portfolio including application platforms, social video, and web browsers.