Global liquidity is the key factor driving Bitcoin prices

I wanted to write down some of the things I’ve been thinking about over and over again, which is how Bitcoin might behave when it experiences a major shift in the flow of funds that has never been seen in its history. I think Bitcoin will have a great trading opportunity once the deleveraging process is over. In this post, I will elaborate on my thoughts.

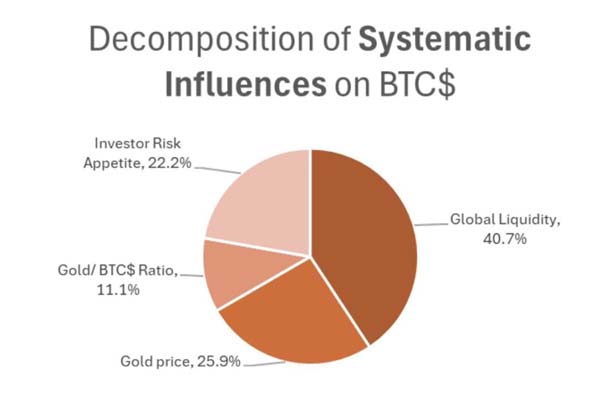

What are the key drivers of Bitcoin price?

I will draw on the research done by Michael Howell on the historical drivers of Bitcoin price action, and then use these results to further understand how the intertwined factors may evolve in the near future.

As shown in the above figure, Bitcoin price is driven by these factors:

Overall investor preference for high-risk, high-beta assets

Correlation between Bitcoin and gold

Global liquidity

My simple framework for understanding risk appetite, gold performance and global liquidity since 2021 is to use fiscal deficit as a percentage of GDP as a quick look at the fiscal stimulus that has dominated global markets since 2021.

Mechanistically, higher fiscal deficits as a percentage of GDP lead to higher inflation, higher nominal GDP, and therefore higher revenues for companies since revenue is a nominal indicator. This is a boon to earnings growth for those companies that can enjoy economies of scale.

For the most part, monetary policy has played second fiddle to fiscal stimulus, which has been the primary driver of risk asset activity. As this frequently updated chart by George Robertson shows, monetary stimulus in the US has been very weak compared to fiscal stimulus, so I will leave monetary stimulus aside for this discussion.

My simple framework for understanding risk appetite, gold performance and global liquidity since 2021 is to use fiscal deficit as a percentage of GDP as a quick look at the fiscal stimulus that has dominated global markets since 2021.

Mechanistically, a higher fiscal deficit as a percentage of GDP leads to higher inflation, higher nominal GDP, and therefore higher revenue for companies since revenue is a nominal indicator. This is a boon to earnings growth for those companies that can enjoy economies of scale.

To a large extent, monetary policy has played second fiddle to fiscal stimulus, which has been the main driver of risk asset activity. As this frequently updated chart by George Robertson shows, monetary stimulus in the US has been very weak compared to fiscal stimulus, so I will leave monetary stimulus aside for this discussion.

The US stock market has been the main marginal driver of risk asset growth, wealth effects, and global liquidity, and has therefore become a gathering place for global capital because capital is treated best in the US. Because of this dynamic of capital inflows into the US, coupled with a large trade deficit, this results in the US exchanging goods for foreign dollars held by foreign countries, which in turn reinvest the dollars in dollar-denominated assets (such as US Treasuries and the "Big Seven" tech stocks)

Now, back to the Michael Howell research mentioned earlier. Over the past decade, risk appetite and global liquidity have been driven primarily by the US, and this trend has accelerated since the pandemic due to the extremely large US fiscal deficit compared to other countries.

Because of this, despite Bitcoin being a globally liquid asset (not just correlated with the US), it has shown a positive correlation with the US stock market, and this correlation has been increasing since 2021.

Now, I believe that this correlation between Bitcoin and the US stock market is spurious. When I use the term "spurious correlation", I mean it in a statistical sense, that is, I believe that a third causal variable that is not shown in the correlation analysis is the real driver. I believe that this factor is global liquidity, which, as we said earlier, has been dominated by the US for nearly a decade.

When we dig into statistical significance, we also have to establish causality, not just positive correlation. Fortunately, Michael Howell has also done some excellent work in this regard, establishing a causal relationship between global liquidity and Bitcoin through a Granger Causality test.

What does this allow us to conclude as a baseline for our further analysis?

The Bitcoin price is primarily driven by global liquidity, and since the US has been the leading factor in global liquidity growth, there is a spurious correlation between Bitcoin and the US stock market.

Over the past month, as we have all speculated on Trump's trade policy goals and the restructuring of global capital and commodity flows, a few major arguments have emerged. I will summarize them below:

The Trump administration wants to reduce trade deficits with other countries, which mechanically means that there will be fewer dollars flowing to foreign countries that would otherwise be reinvested in US assets. If this is to be avoided, the trade deficit cannot be reduced.

The Trump administration believes that foreign currencies are artificially depressed and the US dollar is artificially overvalued, and it wants to rebalance this situation. In short, a weaker dollar and stronger currencies in other countries will lead to higher interest rates in other countries, which will drive capital back to their home countries to capture those interest rate gains, which will be better on a foreign exchange adjusted basis, while also boosting their home stock markets.

Trump’s “shoot first, ask questions later” approach to trade negotiations is driving the rest of the world out of their tiny fiscal deficits relative to the US and into investing in defense, infrastructure, and generally protectionist government investment to make themselves more self-sustaining. Whether or not tariff talks ease (like with China), I think the “genie is out of the bottle” and countries will continue this effort and won’t turn back easily.

Trump wants other countries to increase their defense spending as a percentage of GDP, as the US is shouldering a lot of the costs in this regard. This will also increase fiscal deficits.

I’ll leave my personal opinion on these points aside, as many have already spoken about them, and simply focus on the likely impact of these points if they follow their logic:

Money will leave dollar-denominated assets and flow back to their home countries. This means that US stocks will underperform the rest of the world, bond yields will rise, and the dollar will weaken.

The countries to which these funds are repatriated will no longer have fiscal deficits restricted, and other economies will start spending lavishly and printing money to fill their growing fiscal deficits.

As the US continues to shift from a global capital partner to a protectionist role, holders of US dollar assets will have to increase the risk premium associated with these previously considered high-quality assets and must set wider safety margins for these assets. When this happens, it will lead to higher bond yields and foreign central banks will be interested in diversifying their balance sheets away from relying solely on US Treasuries and towards other neutral assets, such as gold. Similarly, foreign sovereign wealth funds and pension funds may also make such diversification adjustments to their portfolios.

The counter-argument to these views is that the US is the center of innovation and technology-driven growth and no country can replace this position. Europe is too bureaucratic and socialist to develop capitalism like the US. I understand this view and it may mean that this will not be a multi-year trend, but more likely a medium-term trend.

Going back to the title of this article, the first round of transactions is to sell US dollar assets that are overweight globally and avoid the ongoing deleveraging process. With the world so over-allocated to these assets, the deleveraging process could get messy when large money managers and more speculative players with tight stop-loss settings like multi-strategy hedge funds hit their risk limits. When this happens, there will be days like margin calls where a lot of assets will need to be sold to raise cash. Right now, the key is to survive this process and keep enough cash reserves.

However, as the deleveraging process stabilizes, the next round of trading begins. Diversify your portfolio into foreign stocks, foreign bonds, gold, commodities, and even Bitcoin.

We have already started to see this dynamic gradually take shape during market rotations and days without margin calls. The US dollar index (DXY) has fallen, US stocks have underperformed stocks in other parts of the world, gold prices have soared, and Bitcoin has been surprisingly strong relative to traditional US technology stocks.

I think as this happens, the marginal increase in global liquidity will turn to the exact opposite of what we are used to in the past. The rest of the world will take up the mantle of increasing global liquidity and risk appetite.

When I think about the risks of this diversification in the context of a global trade war, I worry about the tail risk of being deeply invested in risk assets in other countries, as there could be some negative headlines about tariffs that could impact these assets. So, in this shift, gold and Bitcoin become my top choices for global diversification.

Gold is currently performing extremely strongly, setting new all-time highs every day. However, while Bitcoin has been surprisingly resilient throughout this shift, its beta correlation with risk appetite has so far limited its gains and failed to keep up with gold's outperformance.

So, as we move toward a global rebalancing of capital, I think the next round of trading opportunities after this round lies in Bitcoin.

When I contrast this framework with Howell's correlation research, I find that they fit each other:

The US stock market is not affected by global liquidity, only by liquidity measured by fiscal stimulus and some capital inflows. However, Bitcoin is a global asset, and it reflects the broad conditions of global liquidity.

As this view gradually gains acceptance and risk allocators continue to rebalance, I think risk appetite will be driven by the rest of the world, not the United States.

Gold couldn’t have done better, and Bitcoin is partially correlated with gold, as we expect.

Putting all of the above together, for the first time in my life, I see the possibility of Bitcoin decoupling from US tech stocks. I know, this is a high-risk idea, and it often marks local highs in Bitcoin prices. But the difference is that this time, the flow of funds may change significantly and lastingly.

So, for a risk-seeking macro trader like me, Bitcoin feels like the most worthwhile trade to participate in after this round of trading. You can’t impose tariffs on Bitcoin, it doesn’t care what country’s borders it is in, it provides high beta returns to the portfolio without the tail risk associated with US tech stocks, I don’t have to judge whether the EU can solve its own problems, and it provides exposure to global liquidity, not just US liquidity.

This market structure is exactly the opportunity for Bitcoin. Once the dust settles on deleveraging, it will be the first to start and accelerate forward.